Effective from April 2023, the Indian government has made it mandatory for companies to maintain an accounting audit trail. The audit trail will help in tracking and maintaining a record of all financial transactions conducted by the company. The audit trail will be helpful in reducing fraud, mismanagement, and embezzlement of funds in companies.

What is an audit trail:

An accounting audit trail is a chronological record of every financial transaction that takes place within a company. It includes information such as the date, time, nature of the transaction, the amount involved, and the parties involved in the transaction. The audit trail ensures that all financial transactions are transparent and can be traced back to their source.

In addition to these requirements, rules also mandate that companies maintain an audit trail of their activities. The audit trail must contain the following details:

- Every transaction that takes place within the company, including the date, amount, and nature of the transaction.

- Every change made to the books of accounts, including the date and nature of the change.

- Every authorization for transaction and changes made to the books of accounts, including the names of the person who authorized them.

- All approvals and rejections of transactions and changes made to the books of accounts, including the names of the person who approved or rejected them.

- Each access to the books of accounts, including the date and time of access and the name of the person who accessed them.

- All backup and restoration activities related to the books of accounts.

The audit trail must be maintained for at least eight years from the end of the financial year for which it pertains. This can help prevent financial irregularities and ensure that the company complies with all relevant laws and regulations.

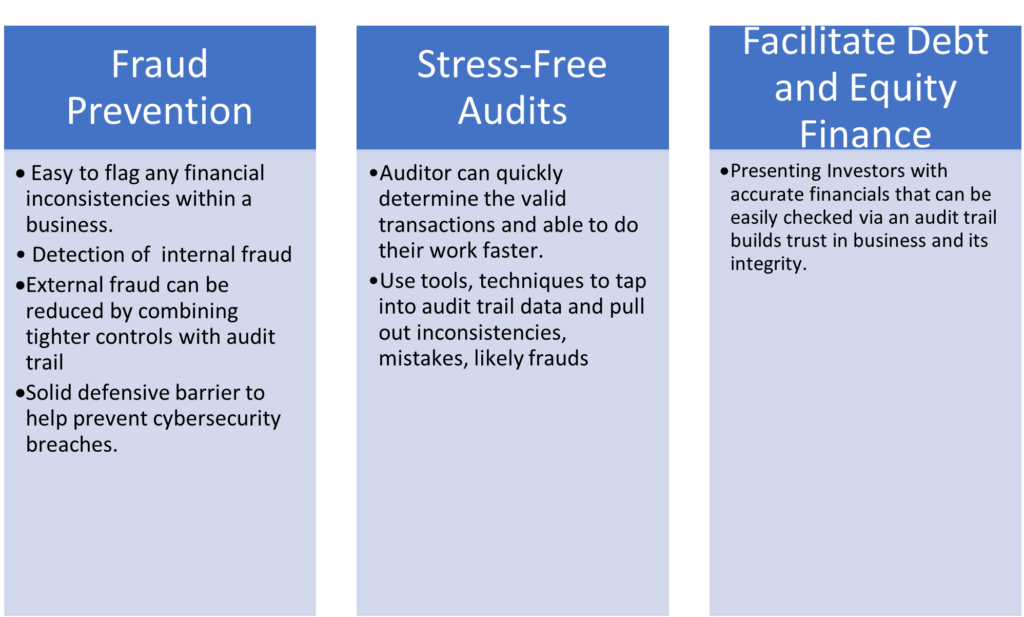

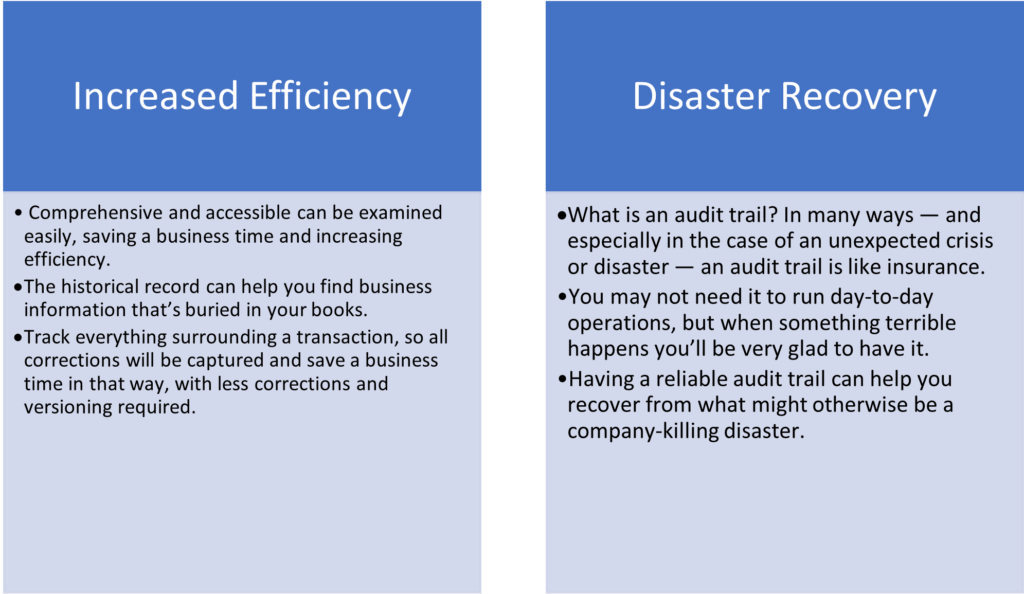

Benefits:

Business Impact & Conclusion

All ERP’S used by companies of varying sizes will make changes to system architecture to adhere to the guidelines. Companies should embrace this change in spite of cost and effort required for compliance so the they are able to get the benefit of transparency, better control, easier fraud detection and increased investor’s interest in the long run.

The accounting audit trail mandatory is a positive step towards improving transparency and accountability in the business environment.

Companies should take this requirement seriously and ensure that they are compliant with the new regulations.

This will help to build trust with their customers, investors, and stakeholders, and promote a more sustainable and ethical business culture in India.

Leave a Reply